Chapter 3.1: Demand and Supply and Market Equilibrium

3.1 Demand Curve, Supply curve, and Equilibrium in Markets for Goods and Services

Learning Objectives

By the end of this section, you will be able to:

- Explain demand, quantity demanded, and the law of demand

- Explain supply, quantity supplied, and the law of supply

- Identify a demand curve and a supply curve

- Explain equilibrium, equilibrium price, and equilibrium quantity

First let’s first focus on what economists mean by demand, what they mean by supply, and then how demand and supply interact in a market.

Demand for Goods and Services

Economists use the term demand to refer to the amount of some good or service consumers are willing and able to purchase at each price. Demand is fundamentally based on needs and wants—if you have no need or want for something, you won’t buy it. While a consumer may be able to differentiate between a need and a want, from an economist’s perspective they are the same thing. Demand is also based on ability to pay. If you cannot pay for it, you have no effective demand. By this definition, a person who does not have a driver’s license has no effective demand for a car.

What a buyer pays for a unit of the specific good or service is called price. The total number of units that consumers would purchase at that price is called the quantity demanded. A rise in price of a good or service almost always decreases the quantity demanded of that good or service. Conversely, a fall in price will increase the quantity demanded. Economists call this inverse relationship between price and quantity demanded the law of demand. The law of demand assumes that all other variables that affect demand (which we explain in the next module) are held constant.

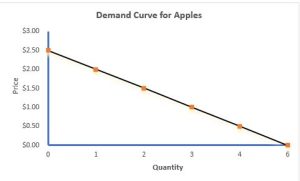

We can show an example for an individual demand curve for apples in a table and a graph. Economists call a table that shows the quantity demanded at each price, such as Table 3.1, a demand schedule. Price is measured in the vertical axis while quantity is measured in the horizontal axis. We start with an individual demand curve for apple for a specific period, for example per week. To start the graph, I asked myself, if the price per apple is $2.50 per apple, how many would I buy? The answer is none. It is too expensive for me. However, for $2.00 I am willing to buy one apple. As the price of apple falls, my quantity demanded for apples increases. A demand curve shows the relationship between price and quantity demanded on a graph like Figure 3.1, with quantity on the horizontal axis and the price per gallon on the vertical axis.

Table 3.1 shows the demand schedule and the graph in Figure 3.2 shows the demand curve. These are two ways to describe the same relationship between price and quantity demanded.

|

Price per apple |

Quantity Demanded |

|

$2.50 |

0 |

|

$2.00 |

1 |

|

$1.50 |

2 |

|

$1.00 |

3 |

|

$0.50 |

4 |

|

0 (free) |

6 |

Table 3.1 Price and Quantity Demanded of Apples

Figure 3.1 A Demand Curve for Apples

The demand schedule shows that as price rises, quantity demanded decreases, and as prices fall quantity demanded rises. We graph these points, and the line connecting them is the demand curve (D). The law of demand states that when price increases, the quantity demanded fall and when price falls, the quantity demanded rises. There is an inverse relationship between prices and quantity demanded.

Demand curves will appear somewhat different for each product. They may appear relatively steep or flat, or they may be straight or curved. Nearly all demand curves share the fundamental similarity that they slope down from left to right. Demand curves embody the law of demand: As the price increases, the quantity demanded decreases, and conversely, as the price decreases, the quantity demanded increases.

Is demand the same as quantity demanded?

In economic terminology, demand is not the same as quantity demanded. When economists talk about demand, they mean the entire curve (= the relationship between a range of prices and the quantities demanded at those prices). When economists talk about quantity demanded, they mean only a single point on the demand curve, or one quantity on the demand schedule. In short, demand refers to the curve and quantity demanded refers to a (specific) point on the curve.

Please note that demand is the entire curve, while quantity demanded is a single point in the curve. Confused about these different types of demand? Read the next Clear It Up feature.

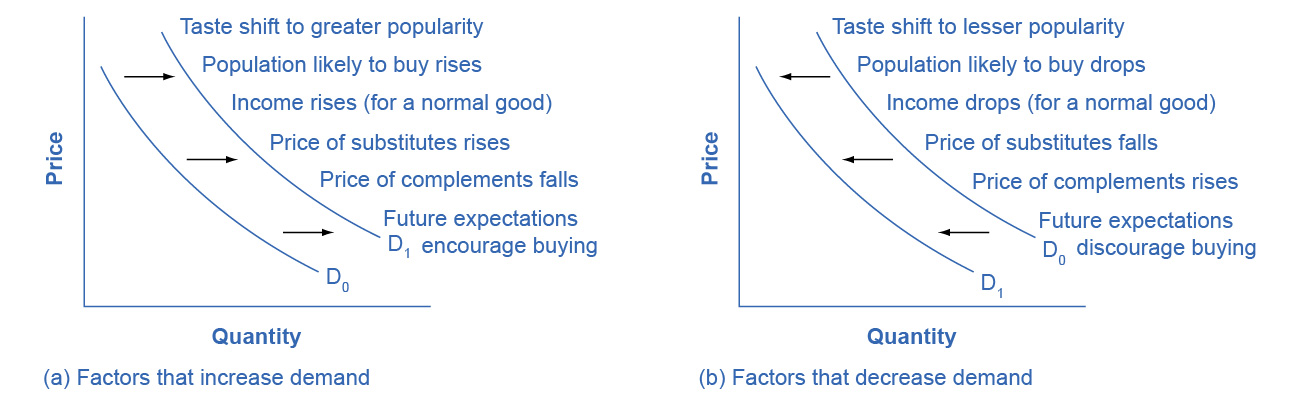

What shifts the demand curve?

If the demand increases, at every price level the quantity demanded increased it is called a shift to the right of the demand curve.

If the demand decreases, at every price level the quantity demanded decreased it is called a shift to the left of the demand curve.

Figure 3.2: Shift of the Demand Curve

What shifts the demand curve?

Income– it depends whether the good is normal or inferior.

Normal Goods- Goods that when income increases the demand increases when income falls the demand decreases.

Inferior Goods- are goods that when income increases the demand falls and when income decreases the demand increases.

Taste and Preferences– If there is a change in taste, the entire demand curve can shift to the right to the left. For example, If doctors discover that aspirin prolongs your life and has tremendous benefits if taking one aspirin a day, then the demand for aspirin will increase and shift to the right.

Prices of related goods -There are two types of goods.

Substitute Goods- goods that can easily substitute each other, for example: Pepsi and Coke.

Complementary Goods- goods that complement each other, for example: French fries and Ketchup.

Expectations of future income– If you expect income to increase and the good is normal, then demand increase (=shift right). – If you expect income to decrease and the good is normal, then demand decreases (=shift left)

Number of consumers– If number of consumer increases, then demand increases (shift right) and if the number of consumers decreases, then demand decrease (=shift left)

Table 3.2 Difference between demand and quantity demanded:

|

Demand |

Quantity Demanded |

|

Demand is a series of points (quantities and prices) that together create a curve |

Quantity demanded is a single point in the curve |

|

All the other factors shift the demand curve to the right or to the left |

Price changes- leads to change in quantity demanded |

|

Other Factors: change in income, change in taste and preferences, change in expectations, change in the prices of substitute or complementary products and change in number of consumers |

P ↑ → Qd↓ and if P↓ → Qd↑ |

|

Shift to the right- increase in demand |

Movement along the curve |

|

Shift to the left- decrease in demand |

|

Supply of Goods and Services

When economists talk about supply, they mean the amount of some good or service a producer is willing to supply at each price. Price is what the producer receives for selling one unit of a good or service. A rise in price almost always leads to an increase in the quantity supplied of that good or service, while a fall in price will decrease the quantity supplied. When the price of apple rises, for example, it encourages profit-seeking apple orchards to take increase production by hiring more workers, buying more ladders and rental picking machinery to increase production. Economists call this the positive relationship between price and quantity supplied—that a higher price leads to a higher quantity supplied and a lower price lead to a lower quantity supplied—the law of supply. The law of supply assumes that all other variables that affect supply (to be explained in the next module) are held constant.

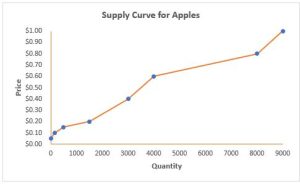

Figure 3.3 illustrates a supply curve for apples. A supply schedule is a table, like Table 3.3, that shows the quantity supplied at a range of different prices. Again, we measure price in dollars in the vertical axis and we measure quantity supplied in the horizontal axis. A supply curve is a graphic illustration of the relationship between price, shown on the vertical axis, and quantity, shown on the horizontal axis. The supply schedule and the supply curve are just two different ways of showing the same information. Notice that the horizontal and vertical axes on the graph for the supply curve are the same as for the demand curve.

Figure 3.3 Supply Curve for Apples

The supply schedule is the table that shows quantity supplied of apples at each price. As price rises, quantity supplied also increases, and vice versa. The supply curve (S) is created by graphing the points from the supply schedule and then connecting them. The upward slope of the supply curve illustrates the law of supply—that a higher price leads to a higher quantity supplied, and vice versa.

|

Price (per apple) |

Quantity Supplied |

|

$0.05 |

0 |

|

$0.10 |

150 |

|

$0.15 |

500 |

|

$0.20 |

1,500 |

|

$0.40 |

3,000 |

|

$0.60 |

4,000 |

|

$0.80 |

8,000 |

|

$1.00 |

9,000 |

Table 3.3 Supply Schedule: Price and Quantity supplied of apples.

The shape of supply curves will vary somewhat according to the product: steeper, flatter, straighter, or curved. Nearly all supply curves, however, share a basic similarity: they slope up from left to right and illustrate the law of supply: as the price rises, say, from $0.20 per apple n to $0.40, the quantity supplied increases from 1,500 apples to 3,000 apples. Conversely, as the price falls, the quantity supplied decreases.

Is supply the same as quantity supplied?

In economic terminology, supply is not the same as quantity supplied. When economists refer to supply, they mean the entire curve- the relationship between a range of prices and the quantities supplied at those prices, a relationship that we can illustrate with a supply curve or a supply schedule. When economists refer to quantity supplied, they mean only a certain point on the supply curve, or one quantity on the supply schedule. In short, supply refers to the curve and quantity supplied refers to a (specific) point on the curve.

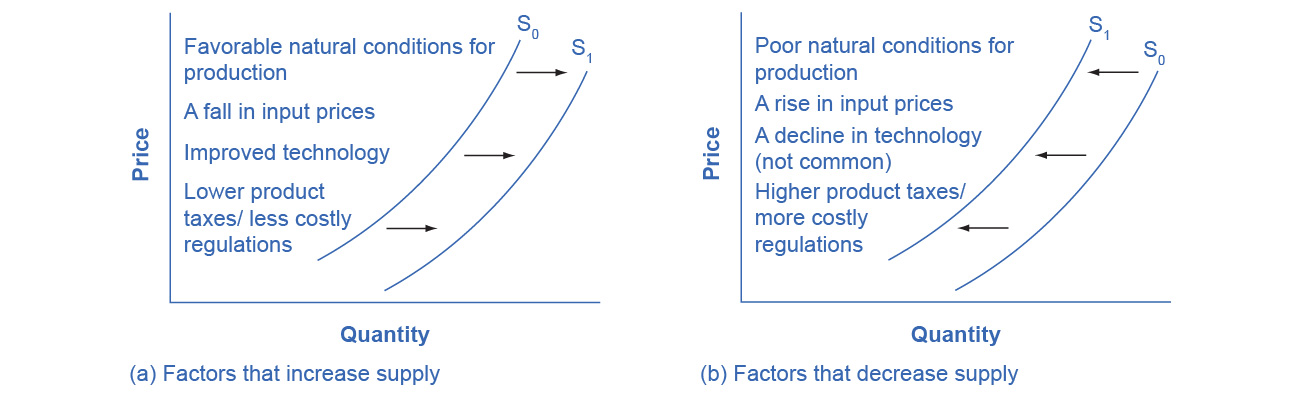

Figure 3.4: Shift of the Supply Curve

What shifts the supply curve?

Cost of Production: If cost of production increases, for example higher wages for workers supply decreases. If cost of production declines, for example through technologies, then supply will increase.

Technology: Advance in technology reduces firms’ costs: increase in supply

Number of Firms: if the number of firms increases, supply increases and if number of firms decreases supply falls.

Table 3.4 Difference between supply and quantity supplied:

|

Supply |

Quantity Supplied |

|

Supply is a series of points (quantities and prices) that together create a curve |

Quantity supplied is a single point in the curve |

|

All the other factors shift the supply curve to the right or to the left |

Price changes- leads to change in quantity supplied |

|

Other Factors: change in prices of inputs, cost of production, change in technology and number of firms |

P ↑ → Qs ↑ and if P↓ → Qs↓ |

|

Shift to the right- increase in supply |

Movement along the curve |

|

Shift to the left- decrease in supply |

|

Equilibrium—Where Demand and Supply Intersect

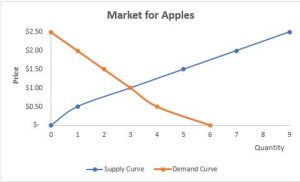

Because the graphs for demand and supply curves both have price on the vertical axis and quantity on the horizontal axis, the demand curve and supply curve for a particular good or service can appear on the same graph. Together, demand and supply determine the price and the quantity that will be bought and sold in a market.

The figure below illustrates the interaction of demand and supply in the market for apples.

Figure 3.5 Market for Apples: Demand and Supply for Apples

The demand curve (D) and the supply curve (S) intersect at the equilibrium point E, with a price of $1.00 and a quantity of 3 apples. The equilibrium price is the only price where quantity demanded is equal to quantity supplied. At a price above equilibrium for example $1.50, quantity supplied exceeds the quantity demanded by 3 units, in other words here is excess supply. At a price below equilibrium such as $0.50, quantity demanded exceeds quantity supplied by 3 units- there is excess demand.

|

Price (per apple) |

Quantity demanded |

Quantity supplied |

|

$0 |

6 |

0 |

|

$0.50 |

4 |

1 |

|

$1.00 |

3 |

3 |

|

$1.50 |

2 |

5 |

|

$2.00 |

1 |

7 |

|

$2.50 |

0 |

9 |

Table 3.5 Price, Quantity Demanded, and Quantity Supplied

Market Equilibrium: is a condition that exists when quantity demanded equals quantity supplied. And NOT demand = supply because demand is a curve going down and supply a curve going up.

Remember this: When two lines on a diagram cross, this intersection usually means something. The point where the supply curve (S) and the demand curve (D) cross, designated by point E in Figure 3.5, is called the equilibrium. The equilibrium price is the only price where the plans of consumers and the plans of producers agree—that is, where the amount of the product consumers want to buy (quantity demanded) is equal to the amount producers want to sell (quantity supplied). Economists call this common quantity the equilibrium quantity. At any other price, the quantity demanded does not equal the quantity supplied, so the market is not in equilibrium at that price.

In Figure 3.5, the equilibrium price is $1.00 per apple and the equilibrium quantity is 3 apples. s. If you had only the demand and supply schedules, and not the graph, you could find the equilibrium by looking for the price level on the tables where the quantity demanded and the quantity supplied are equal.

The word “equilibrium” means “balance.” If a market is at its equilibrium price and quantity, then it has no reason to move away from that point. However, if a market is not at equilibrium, then economic pressures arise to move the market toward the equilibrium price and the equilibrium quantity.

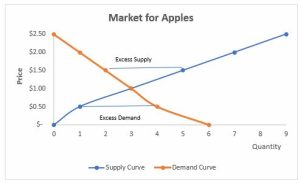

Excess Supply and Excess Demand

Excess Supply exists when the amount supplied exceeds the amount demanded. This is also known as a surplus. At this point, suppliers must lower their price and that will cause for a lower price in which in turn demand will rise and an equilibrium will be created.

Imagine, for example, that the price of an apple was above the equilibrium price—that is, instead of $1.00 the price is $1.50 per apple. The dashed horizontal line at the price of $1.50 in Figure 3.6 illustrates this above-equilibrium price. At this higher price, the quantity demanded drops from 3 units to 2 units. This decline in quantity reflects how consumers react to the higher price of apples and perhaps buying substitute to apples.

Moreover, at this higher price of $1.50, the quantity of apples supplied rises from 3 units to 5 units, as the higher price makes it more profitable for apples producers to expand their output. When the quantity supplied is higher than the quantity demanded we call this an excess supply or a surplus.

When the quantity supplied is 5 units and the quantity demanded only 2 units this is a surplus or excess supply of 3 units.

Excess Demand exists when quantity demanded is greater than the quantity supplied at the current price. This is also known as a shortage. At this point, the prices rise, and the quantity demanded goes down, and those who are willing to pay a higher price will. At the same time, suppliers are happy with the higher price they increase quantity supplied, and where the price axis intersect with the quantity axis, a new equilibrium is created.

Now suppose that the price is below its equilibrium level at $0.50 per apple, as the dashed horizontal line at this price in Figure 3.6 shows. At this lower price, the quantity demanded increases from 3 units to 4 units. However, the below-equilibrium price reduces the quantity supplied of apples from 3 units to one unit. Thus, creating an excess demand of 3 units.

Figure 3.6 Illustrates excess supply and excess demand in the market for apples.

Changes in Market Equilibrium

According to the example above, there always will be forces pushing the market towards equilibrium. If the price of apples is above $1.00 per apple, there will be excess supply putting pressure for the price of apples to decrease. And, if the price of apples is too low creating excess demand or a shortage, there will be pressure to increase the price to apples until it reaches equilibrium again at $1 per apple and 3 apples are bought and sold. The question is; is the price of apples for ever and ever will be $1 per apples, or are there any circumstances in life that could change the price of apple?

The answer is that changes in market equilibrium occurs when a shift in either the demand curve or the supply curve takes place. We spoke about the things that cause a shift in the demand curve and in the supply curve. If any of these factors changes, the price and equilibrium of apples will change too.

This chapter is a remixed version of the chapters 3.1 Demand, Supply, and Equilibrium in Markets for Goods and Services in Principles of Macroeconomics 3e by OpenStax, published under a Creative Commons Attribution 4.0 International License. Other additions and modifications have been made in accord with the style, structure, and audience of this guide.